Variable Rate Investment Loan

From

Variable rate

Comparison rate*

Why choose a Variable Rate Investment Loan?

Free redraw

100% offset account

Borrow up to 90%

No ongoing fees

The investment loan features don't stop there

- Competitive variable interest rate.

- No ongoing monthly or annual fees.

- Open up to three 100% offset accounts so your savings can reduce the amount of interest you pay on your home loan.

- Choose to repay weekly, fortnightly, or monthly.

- Choose interest only or principal and interest repayments.

- Make extra payments without penalty, so you can own your investment property sooner.

- Access your additional repayments and redraw online if you’re ahead.

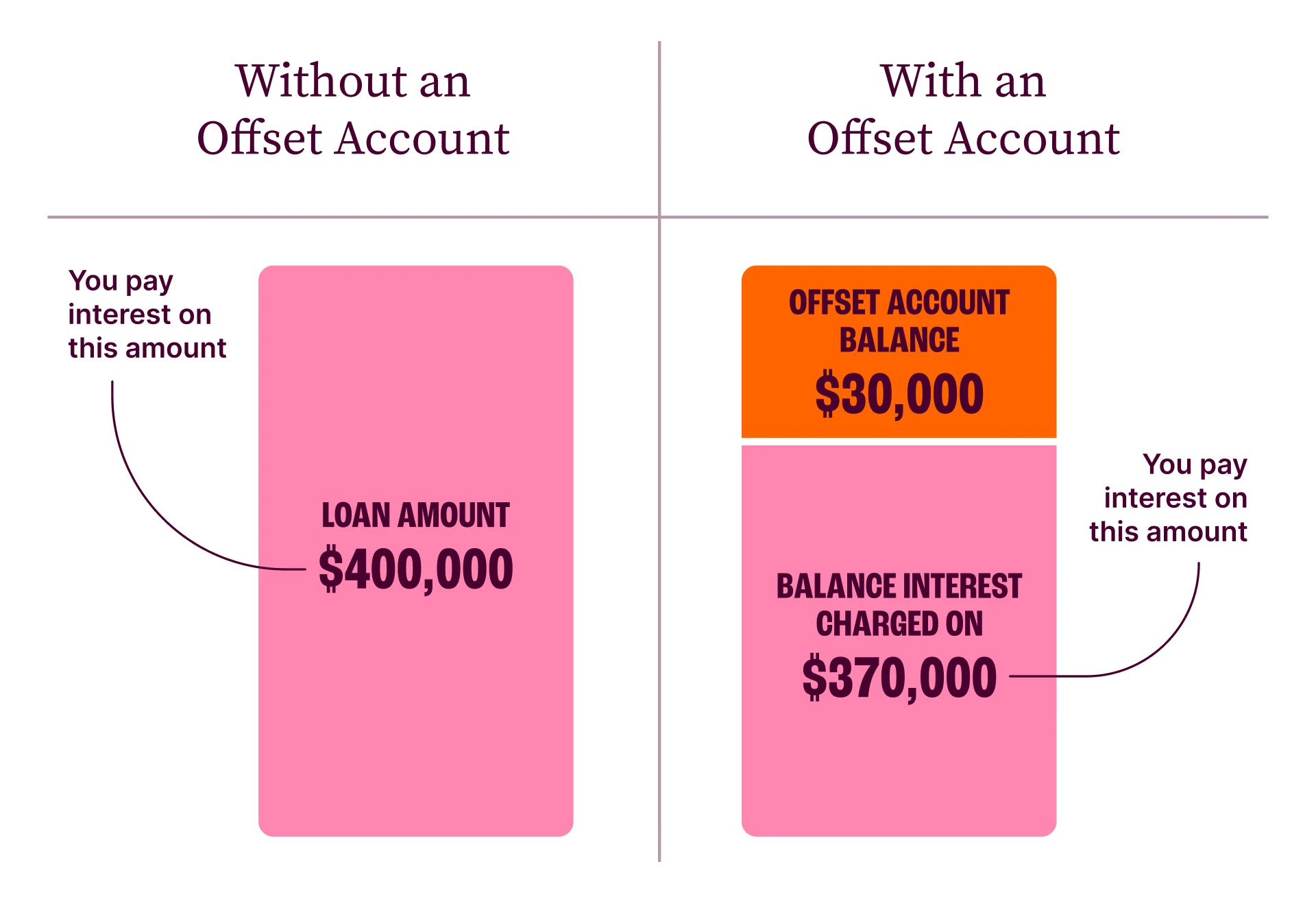

How an offset account works

An offset account is a transaction account linked to your home loan. Every dollar in the account is offset against your home loan balance, which reduces the amount of interest you pay each month.

For example, if you have $30,000 in your offset account, and a loan balance of $400,000, you’ll only be charged interest on $370,000. Every dollar you save on interest adds up over time, helping you to save thousands over the life of your loan.

Plus, if you have your salary paid into your offset account, every dollar you earn will work in your favour until it’s spent.

Rates and fees

The basics

| Loan purpose | Investment |

| Minimum loan amount | $20,000 |

| Maximum loan term | 30 years |

| Optional linked offset account | Mortgage Offset Saver Account |

Interest rates

| Loan to Value Ratio (LVR) | Repayments | Variable rate |

Comparison rate*

|

|---|---|---|---|

| Less than 90%^ | P&I | 6.44% p.a. | 6.47% p.a. |

| Less than 90%^ | IO | 7.62% p.a. | 6.81% p.a. |

| Fee type | |

|---|---|

| Monthly fee | $0.00 |

| Annual fee | $0.00 |

| Document preparation fee | $300.00 |

| Switch fee (from other BCU Bank loan) | $300.00 |

Other fees & charges that apply to all of our accounts can be found on our fees and charges page.

How much could you borrow?

Use our handy home loan borrowing power calculator to get an idea of much you could potentially borrow. We’ll just need the basics about what you earn, spend, and owe, and we’ll figure out the rest.

Home loan borrowing power calculator

More calculators

Ready to apply for a home loan?

It’s easy to get started with a BCU Bank home loan. Choose the way that suits you:

- In your nearest branch – remember to bring all your ID and supporting documents with you.

- Over the phone – call us on 1300 228 228 and one of our friendly consultants will help you with your home loan application.

- At home or at work – our mobile lending team can meet at a time and place that suits you, or we can set up a video call.

A little preparation can make your home loan application quicker and easier. Make sure you have the following ready:

- Identity documents

- primary photo ID (e.g. passport or driver licence), or

- primary ID without a photo (e.g. birth certificate or citizenship certificate) and a secondary ID (e.g. utility bill with your name and address on it).

- Employment details – contact details of your current and previous employer (if current is less than two years).

- Income details – payslips or, if you're self-employed, tax assessments for the last two years, and financial statements.

- Regular expenses – such as rent, food, electricity, insurance, telcos, and medical costs.

- Assets – a rundown of any assets that you own (any cars, savings accounts, home contents, properties, investments).

- Liabilities – the details of any loans, credit cards, buy now pay later, or other debts you have.

Got everything ready? Book an appointment with one of our home loan specialists today.

Request an appointmentIt’s easy to get started with a BCU Bank home loan. Choose the way that suits you:

- In your nearest branch – remember to bring all your ID and supporting documents with you.

- Over the phone – call us on 1300 228 228 and one of our friendly consultants will help you with your home loan application.

- At home or at work – our mobile lending team can meet at a time and place that suits you, or we can set up a video call.

Because we're here to help

We'll call you

Talk to the team

We’ll come to you

Got a question about home loans?

Principal and interest repayments are when you pay off a portion of the principal balance of the loan (the amount you originally borrowed) plus the interest charges with every repayment you make.

Interest only repayments are as the name suggests - you're repaying the home loan interest charges only, calculated over your loan term and charged monthly. You'll not be paying off any of the principal balance of the loan. Interest only payments apply for an initial maximum period of five years.

Principal and interest repayments will apply once an interest only term has matured. You'll receive plenty of notice on your maturing interest only period and what your new principal and interest repayments will be. This will give you an opportunity to review your lending facilities.

You can have up to three Mortgage Offset Saver accounts (whether in single or joint names) in total linked to an eligible home loan.

These accounts must be in the name of one or more (or all) of the home loan borrowers.

There are many tax implications to consider if you’re buying and maintaining an investment property.

The income you receive from the property may be tax deductible, likewise for the costs of managing the property. Then there’s tax on any profit you make if you sell the property.

Before doing anything we recommend that you speak to your accountant or a financial advisor, to understand if buying an investment property is right for you.

LVR stands for Loan to Value Ratio. This is calculated as the amount you want to borrow as a percentage of the value of the property you buy, or that will be used as security.

For example, if you borrow $540,000 to buy a property valued at $600,000, your LVR would be 90%.

Important information

Banking and Credit products issued by Police & Nurses Limited (BCU Bank).

Any information on this website is general in nature and does not consider your personal needs, objectives or financial situation. Our rates are current as of today and can change at any time. Eligibility criteria, terms and conditions, fees and charges apply.

Please consider the terms and conditions and whether a product is right for you.

- View the home loans terms and conditions

- View the home loan fees and charges

- View Credit Guide

- Create a Home Loan Key Fact Sheet

- View LMI Information Fact Sheet

- View Target Market Determinations (TMDs)

*Comparison rate calculated on a loan amount of $150,000 over a term of 25 years based on monthly repayments. For variable Interest Only loans, comparison rates are based on an initial 3 year Interest Only period. For fixed Interest Only loans, comparison rates are based on an initial Interest Only period equal in length to the fixed period. During an Interest Only period, your Interest Only payments will not reduce your loan balance. This may mean you pay more interest over the life of the loan.

WARNING: This comparison rate applies only to the example or examples given. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or early repayment fees, and cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan.

^If you are borrowing more than 80% of the property’s value (Loan to Value Ratio), Lenders Mortgage Insurance (LMI) may be required. Borrowing up to 95% includes LMI costs.